Car Insurance Coverage

If you own a car, you buy car insurance coverage. In the process, you have to make lots of decisions. Do you want to buy Comprehensive? Collision? What limit for Bodily Injury? For Medical Payments? For Uninsured Motorist? What deductible? As with other insurance products, auto insurance is full of its own unique terminology. In this post, I’ll explain all these terms and provide some insights on how to make some of the decisions that determine your car insurance coverage.

As I told my kids (see Advice I Gave My Kids post), I recommend that you read every contract before you sign it. Auto insurance policies don’t change all that much from year to year. If you use the same insurer and live in the same state, you can probably read the policy every few years to refresh your memory. In the meantime, this post will help you understanding the basics.Before going into the coverages, though, I need to provide some background about liability and different types of laws governing the liability for car accidents.

No-Fault vs. Tort Jurisdictions

When you cause an accident in which someone else is hurt or their property is damaged, you have created a liability for yourself to reimburse them for their economic loss. That is, you are liable for paying their medical costs and lost wages, among other things, and repairing or replacing their property. In some 12 states (see the chart at the end of this article for a list) and most or all of Canada, though, the laws make the driver of each car involved responsible for their own and their passengers’ costs in certain accidents.In the 1970s, car insurance costs escalated very rapidly. No-fault coverage was introduced in some jurisdictions to slow auto insurance inflation. In theory, under a no-fault system, every driver is responsible for the costs of themselves and their passengers regardless of who was at fault for the accident. In practice, no-fault is applied to only “small” accidents. The definition of “small” varies widely across jurisdictions, with some defining it based on the total cost of injuries and damage and others based on the nature of the injury. Jurisdictions that don’t have a no-fault system are often called tort jurisdictions.

Tort Liability

In a tort jurisdiction, you are required to buy Bodily Injury liability coverage. In these jurisdictions, this coverage protects you against the cost of all injuries to others. You will also be offered Medical Payments coverage which reimburses you for your and your passengers’ medical costs in accidents you cause.

No-Fault

Under a no-fault system, you are also required to buy Bodily Injury liability coverage to protect yourself against the cost of injuries to others, but only for accidents that aren’t “small.” In addition, you will be offered Personal Injury Protection which covers injuries to you and your passengers in accidents you cause and in all “small” accidents caused by others.

Coverage Overview

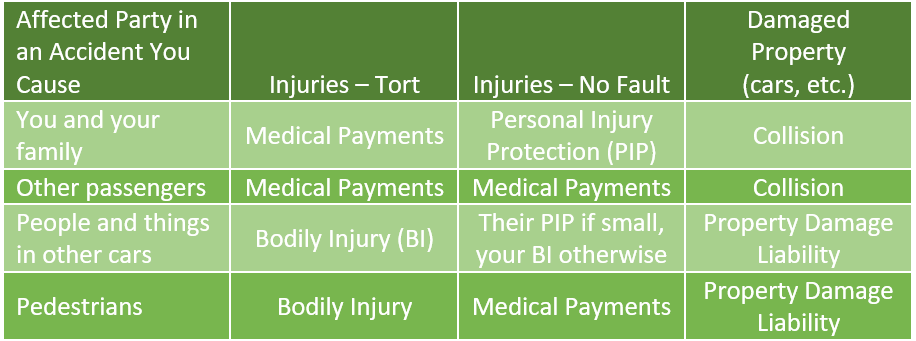

The table below shows which of your coverages will protect you against costs from the people injured and property damaged or destroyed in an accident you cause. I’ll describe these insurance coverages in a bit more detail below.

Your insurance coverage is available to you regardless of whether you are driving your car or someone else’s car, including rental cars. If you purchase Collision coverage, it will be cover the full amount of damage for any other vehicle you drive even if the other vehicle is worth more than any of your cars.

Your coverage is also available to anyone else who is driving your car with your permission. That is, unless someone steals your car, all of the coverages that you buy are available to another driver. Loss or damage to your car due to theft is covered under Comprehensive.

Bodily Injury Liability (BI)

Bodily Injury liability coverage pays costs related to injury or death for which you become legally responsible because of a car accident. Interestingly, passengers are not insured under Bodily Injury liability coverage but rather are covered under your Personal Injury Protection, Medical Payments or Uninsured Motorist coverage. In no-fault states, the insurer pays only when the accident is severe enough to not be considered small.

Property Damage Liability

Property damage liability coverage pays the cost of damage to other people’s cars and property for which you become legally liable. Most of the time, the damage is to other people’s cars and their contents. I know one person, though, who fell asleep while driving in a rural area. She crossed the median, the lanes in the other direction and ran into the front of a store. Fortunately, no one was injured, but the store and its contents were damaged. In this accident, her car insurer repaired the store and replaced its contents under her Property Damage liability coverage.

Liability Limits

You will have the option to select the limit of liability for your Bodily Injury and Property Damage liability coverages. Coverage can be offered with split limits or a combined single limit (CSL).

Split Limits

When there are split limits, you will see three numbers, e.g., $100K/$300K/$50K. The first number ($100,000 in the example) refers to the amount the insurer will pay for each injured person. The second number ($300,000 in this example) is the total amount the insurer will pay for Bodily Injury coverage for each accident. The third number ($50,000) is the total amount it will pay per accident for Property Damage liability.

Combined Single Limit

When there is a combined single limit, the limit will be described using a single number. That number is the maximum amount the insurer will pay for each accident for all injuries and Property Damage liability combined.

I usually buy a combined single limit, but recommend looking at different options to compare the pricing. For example, if you can find $100K/$300K/$50K coverage for significantly less than a $300,000 combined single limit, you might want to buy the split limits. I buy the combined single limit because there is more coverage if a single person is severely injured. For example, if only one person is injured in an accident I cause but that person has $250,000 of medical costs and lost wages, a $100K/$300K/$50K limit would cover only $100,000 of the $250,000. A $300,000 combined single limit policy would cover all of it. Another reason I buy a combined single limit is that I buy an umbrella policy (which I’ll cover in a future post). My umbrella policy requires a combined single limit on my underlying auto policy.

What Limit

I always buy as much limit as I can afford (and, as I indicated above, started buying umbrella insurance when I could afford it). If you injure someone severely in an accident, you are liable for the full amount of their medical costs and lost wages regardless of whether they are covered by insurance. If someone has $250,000 of medical expenses and lost wages and the applicable limit on your policy is $100,000, they can demand that you pay the remaining $150,000 from your personal assets.

Personal Injury Protection (PIP)

Personal Injury Protection coverage (PIP) pays benefits to you and members of your immediate family when involved in an auto accident, regardless of who is at fault, in a no-fault jurisdiction. You can be reimbursed for medical expenses, loss of income and funeral expenses. When I lived in a no-fault state, I bought a much lower limit for Personal Injury Protection than for Bodily Injury liability. Most importantly, my family and I have always had health insurance and I had disability coverage. If you are severely injured in a car accident, your auto insurer pays first. My health and disability insurance also provided coverage after my auto insurance coverage was exhausted. I suggest confirming with your human resources contact or health and disability insurers that you would be covered if injured in a car accident before making the same choice I did. If not, you might want to consider buying as high a limit as you can afford.

Medical Payments

Medical Payments coverage reimburses medical expenses in an accident. In all states, coverage is provided for passengers who are not family members and pedestrians. In tort states, you and your family members are also covered.

I probably don’t buy a high enough Medical Payments limit. Until I wrote this post, I always focused primarily on my situation and selected my limit in the same way I did my Personal Injury Protection limit. Now that I’ve thought about it more, I realize that I should also be considering my passengers and any pedestrians I might injure. They might not have as much health and disability insurance as I do, so I wouldn’t have a back-up if my Medical Payments limit was less than the cost of their medical care and lost wages. If you have a lot of non-family-member passengers and especially if you drive other people’s children to school or activities, you might want to consider buying as much Medical Payments limit as you can afford.

Uninsured and Underinsured Motorist (UM/UIM) Coverage

If you, your family members or your passengers are injured in an accident caused by someone else, that person is liable for your medical costs and lost wages. Unfortunately, there are many accidents in which the other driver’s Bodily Injury limit is less than your medical costs and lost wages or sometimes the other driver has no insurance at all (which is illegal in all US states and Canadian provinces, but still happens). In those situations, your insurer will reimburse you for any costs you can’t recover from the other driver or its insurance under your Uninsured and Underinsured Motorist (UM/UIM) coverage. The maximum amount you can receive from your insurer is your UM/UIM limit. Your insurer then has the right to try to recover any amounts it pays to you from the other driver directly.The selection of a UM/UIM limit is very similar to that of a Medical Payments limit in that you are buying protection for not only you and your family members, but also your passengers.

Physical Damage Coverages

Damage to your car from accidents you cause can be insured under Collision and Comprehensive coverages.

Collision and Comprehensive

Collision reimburses you for damage to your car when it impacts another vehicle or object or rolls over. Comprehensive reimburses you for damage to or loss of your car from perils than a collision. Perils explicitly covered by Comprehensive are:

Missiles or falling objects

Fire

Theft

Explosion or earthquake

Windstorm

Hail, water or flood

Malicious mischief or vandalism

Riot or civil commotion

Contact with bird or animal

Breakage of glass (also covered under Collision if from an accident)

In addition, many policies will also reimburse you for a temporary replacement for your vehicle until it is repaired. My policy provides only $20 a day up to a maximum of $600, so the coverage would help cover the cost of renting a car but is not likely to be enough.

A quick tip – Property Damage liability coverage is easily confused with physical damage coverage. Property damage liability covers other people’s cars. Physical damage coverage includes Collision and Comprehensive so protects your car.

I have an example to illustrate the difference. One of my daughter’s friends was driving back to college late at night after Thanksgiving on an interstate. She hit a deer and totaled her car. She had not purchased Comprehensive, so was afraid she was going to have to figure out how to replace her car on a very limited budget. It turns out the deer had a hunter’s tag on it and had fallen off the roof of the hunter’s car. Because the hunter was responsible for the deer being in the road, she was fully reimbursed for the value of her car under his Property Damage liability coverage.

Physical Damage - What to Buy

Collision and Comprehensive coverages can be quite expensive. On one of my recent policies, my Comprehensive coverage cost more than my liability coverages, while my Collision coverage cost is 2/3 of the cost of my liability coverages. I note that I have selected a high deductible and drive moderately old cars. These coverages would be even more expensive if I drove newer cars or selected a lower deductible. As such, it is very important to balance the benefits of these coverages with their cost.

Physical Damage - Rules of Thumb

I have a few rules of thumb I use in making my decision about whether to buy Comprehensive and Collision coverage and at what deductibles. They are:

Never buy insurance on something you can afford to lose or replace. For example, you might have an old beater car you drive only in the winter. If you can afford to replace the car or have another car you can drive in the winter, you might not buy Collision or Comprehensive on that car at all.

Select the highest deductible you can afford. If you can’t afford to replace your car, especially if it is new or your only vehicle, you’ll want to buy Comprehensive and Collision if it fits in your budget. You can reduce the cost of these coverages by selecting a higher deductible. You can review your budget and your savings to see how much you can afford to repair or replace a vehicle if it is damaged or stolen. This review can inform your selection of a deductible.

Always put Comprehensive and Collision on at least one car if you rent cars for personal use with any frequency. As mentioned below, your car insurance will cover you when you rent a car up to the maximum coverage you have on any one vehicle. If you rent cars for only a few days a year, the cost of the rental car company’s insurance will be less than the cost to cover one of your cars for physical damage. My experience, though, is that rental-car companies’ insurance is very expensive and I can afford to put Comprehensive and Collision coverage on one of my cars for my annual cost of buying coverage on rental cars.

Towing and Labor

Some insurers offer to insure you against the costs of towing and labor if your car breaks down. Examples of the labor costs that are insured under this coverage include unlocking your car, changing a tire, gas, oil or water delivery, and jump-starting your car. To be clear, your car insurer will not pay for any repairs to your car once it has been towed. It just covers costs to get you off the side of the road. This coverage is very similar to what is available from such entities as the American Automobile Association (AAA) or the Canadian Automobile Association (CAA). If you are interested in this coverage, you’ll want to compare the coverage and cost from your insurer with that from other entities. For example, depending on what level of service you buy, AAA will tow your car for either five or 100 miles. By comparison, towing coverage under a personal auto policy is capped at the dollar amount of the limit you purchase. As you make the cost comparison, you’ll want to consider whether you use any “free” services from the other entities. Also, if you buy this coverage, remember to use it if you find yourself stranded. I was so rattled by being forced off the road and onto the median by a truck in a couple feet of snow that I forgot I had this coverage. I ended up paying the tow bill myself. Oops!

Exclusions

There are lots of exclusions in an auto policy. Some important exclusions I have seen include:

You are not covered for intentional acts. For example, if you are mad at another driver and intentionally run your car into the other driver’s car, your insurance company won’t pay for any damage or injuries.

You are generally not covered if you are using your car in a business related to cars. Driving your car for Uber or Lyft or similar is almost always excluded. Also, if you park, sell or repair cars, any damage to or caused by those vehicles will not be covered.

You are usually not covered if you are driving a vehicle other than a car, pickup or van for any type of work.

You are not covered for injury to anyone who is your employee, unless it is a domestic employee. We always added our nannies on our insurance policies as drivers to make sure there was no question that they were covered.

Tips about Renting Cars

Your auto policy will cover you and a rental car in the same way as it covers the vehicle on your policy that has the greatest coverage. For example, let’s say you own two cars – a new one with $500-deductible Comprehensive and Collision coverage and an old one with no physical damage coverage. Your insurer will provide $500-deductible Comprehensive and Collision on any cars you rent.

The one exception is that many insurers won’t cover the charges from the rental company for the loss of use of its vehicle. That is, the rental company charges the renter for the costs it incurs and the profits it loses because the car is being repaired and not available for rent. These charges are known as loss-of-use charges. These charges can be very expensive, even more than the costs to repair the car.

In all our years of renting cars, we have only had one claim. One of our nannies left her purse in plain sight in a locked rental car when she took the kids to the beach. Someone broke the back passenger window to grab her purse. In that case, our insurer paid for the damage to the car under our Comprehensive coverage after we paid the deductible. It also argued with the rental car company about the loss-of-use charges. In the end, we did not have to pay anything other than our deductible.When renting cars, I decline all of the insurance coverage offered, taking my risk that I might have to pay for loss of use. But, I also make sure I always have Comprehensive and Collision on at least one car so that coverage and, even more importantly, the insurer’s leverage in negotiating with the car rental company are available when I rent cars.